A wave of confident tax advice is moving through Bali’s property channels right now, and a good deal of it is wrong. The loudest version runs like this: Indonesia has raised tax from 0.5 per cent to 22 per cent, so foreign buyers should stop opening a PT PMA and think hard about buying at all. It has been repeated in reels, forwarded through WhatsApp groups, and stated as settled fact by people who have not read the regulation. The regulation is real. The conclusion drawn from it is not.

What the Regulation Actually Changed

The regulation is Government Regulation Number 20 of 2026, which amends Number 55 of 2022, and it took effect on 22 April 2026. It did not raise a single rate. It narrowed who may use the 0.5 per cent final tax on gross turnover, a simplified scheme built for genuinely small businesses. That facility now stays open to individuals, single-shareholder PT Perorangan, and cooperatives, under a turnover ceiling of IDR 4.8 billion. Ordinary companies, the standard PT, the CV, the firm, move to the normal corporate regime.

That regime is 22 per cent on net profit, reduced to an effective 11 per cent under Article 31E for companies turning over less than IDR 50 billion. None of those figures is new. The 22 per cent has been in place since 2022. The 11 per cent relief has sat beside it the whole time. Nothing was raised. Eligibility was tightened.

The Comparison That Falls Apart on Inspection

Here is what the headline comparison hides. The 0.5 per cent is charged on gross turnover. The 11 and 22 per cent are charged on net profit, after legitimate costs are deducted. Setting one against the other as though a business simply moved from paying 0.5 to paying 22 of the same figure is not a comparison at all. It is a category error.

Adv. Surya Dharma SH., CPL., Director of 4 Pillars Consulting, puts the more important point plainly. The 0.5 per cent scheme was never intended for the commercial villa accommodation business in the first place, whether the operator is Indonesian or foreign. It is a local small-business incentive, designed for home industry, food and beverage, and small services. A villa rental operation, and certainly a foreign-owned PT PMA, sat outside it from the start. So the buyer being told to abandon a PT PMA over a tax rise never had a 0.5 per cent rate to lose. That structure was always taxed on the normal regime. For the villa buyer, nothing changed.

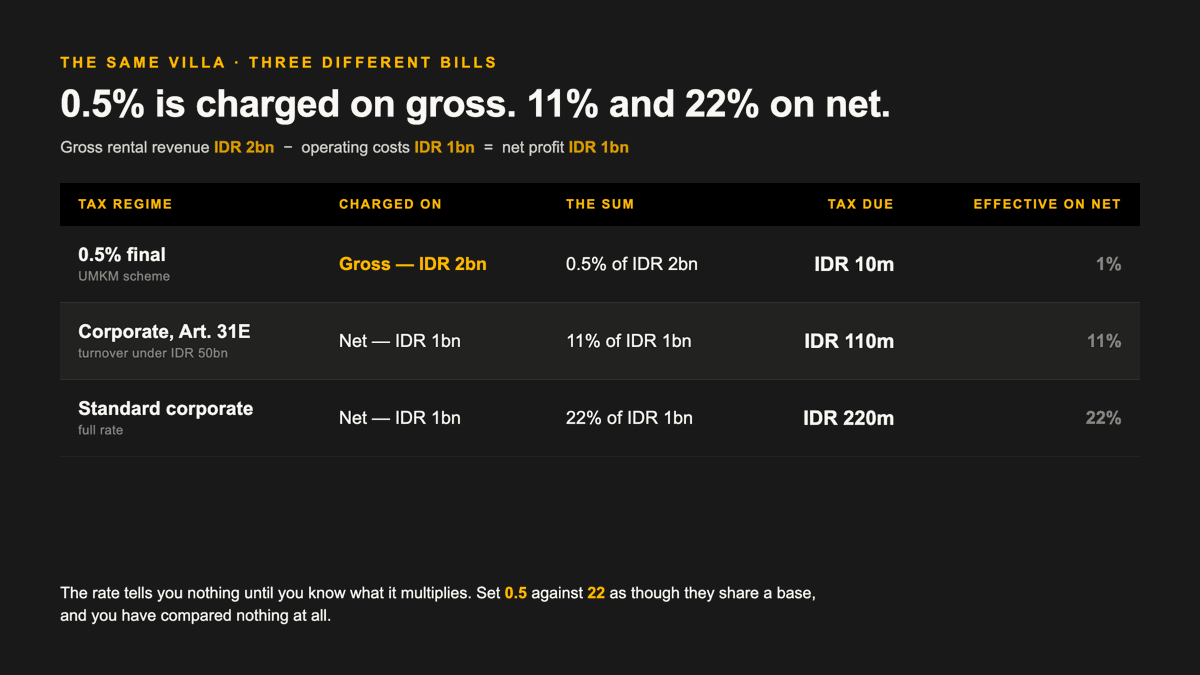

The Same Villa, Three Different Bills

The comparison falls apart the moment you do the arithmetic, and the arithmetic takes about ten seconds. Almost nobody repeating it has bothered.

Surya ran the same rental business under all three figures. Start with the business. Annual gross rental revenue of IDR 2 billion. Deductible operating costs of IDR 1 billion, across staff, utilities, repairs, agency commissions, marketing and administration. Take one from the other and the net profit is IDR 1 billion.

Now apply each regime, and watch what each one is actually multiplied against.

The 0.5 per cent final tax is charged on gross revenue. The sum is 0.5% of IDR 2,000,000,000, which is IDR 10,000,000.

The corporate regime is charged on net profit, not revenue. At the effective 11 per cent under Article 31E, the sum is 11% of IDR 1,000,000,000, which is IDR 110,000,000. At the full 22 per cent, it is 22% of IDR 1,000,000,000, which is IDR 220,000,000.

| Tax regime | The sum | Tax due | Effective rate on net profit |

| 0.5% final (UMKM) | 0.5% of 2bn gross | IDR 10 million | 1% |

| Corporate, Article 31E | 11% of 1bn net | IDR 110 million | 11% |

| Standard corporate | 22% of 1bn net | IDR 220 million | 22% |

The two taxes are not looking at the same number. One takes its slice from the whole IDR 2 billion of turnover. The other takes its slice from the IDR 1 billion of profit that survives after costs. Set 0.5 against 22 as though they share a base, and you have compared nothing at all.

Then change one thing. Hold revenue at IDR 2 billion, but lift costs to IDR 1.85 billion, so the profit left is IDR 150 million. The corporate figures fall with the profit. The 0.5 per cent figure does not move, because it never looked at profit in the first place. It is still 0.5% of IDR 2,000,000,000, still IDR 10,000,000. Except that IDR 10 million is now being paid out of IDR 150 million of profit, which is an effective 6.67 per cent, not the comfortable 1 per cent it looked like a moment ago.

| Tax regime | Tax due | Effective rate on net profit |

| 0.5% final (UMKM) | IDR 10 million | 6.67% |

| Corporate, Article 31E | IDR 16.5 million | 11% |

| Standard corporate | IDR 33 million | 22% |

That is the entire lesson in two sums. The most efficient regime is not the one with the smallest number on the poster. It is the one whose base, gross or net, suits the margin the business actually runs at. The rate tells you nothing until you know what it is multiplied by.

Surya is careful to add that this models corporate income tax alone, not the full tax picture. Other charges sit outside it, including taxes collected from guests and merely administered by the operator, which should never be confused with the tax the business itself bears.

The Tax Nobody Mentions Until the Deal Is Done

This is where the real risk lives, and it is not in the number being argued about online. It is in the figures nobody raises until the deal is almost closed. Buyers fix on the asking price and treat tax as paperwork for later. Tax is the silent killer of property deals, the cost that surfaces after everyone has shaken hands and quietly decides whether the purchase ever made sense.

What a villa actually carries depends on questions most buyers never ask. Surya draws a distinction that reframes the whole exercise: the same villa is taxed differently depending on whether the taxpayer is the owner of the property, the operator of the business, or both. A short-term daily rental run through a company follows the corporate regime. The same villa let on a mid or long-term basis is taxed on the owner at 10 per cent final on the gross rent, a simpler and often lighter position. The model determines the tax, and the model is a decision made before the purchase, not after.

The Questions That Belong Before the Deposit

There are tax questions that belong at the very start of a search, not the end. Each one is ordinary diligence, and each one is far cheaper to ask than to discover late.

Is VAT included in the quoted price, or does it sit on top? On a new developer purchase this can move the real cost materially. Our standard at Fullers is to settle this in writing first, and to require the quoted price to be the price inclusive, not a figure that grows at signing.

Who carries the tax on the transfer, and does the form of the sale change it? A leasehold, a freehold, and a sale of company shares are each taxed differently, and each shifts the burden in ways that are only negotiable before you commit.

Does the seller hold the property personally or through a company? The answer changes which taxes apply and who pays them.

Is a resale taxed differently from a new purchase from a developer? It can be, and that difference is rarely volunteered.

What is the ongoing tax position once you own and operate under your intended model? A daily-let plan and a long-stay plan do not carry the same obligations.

As Surya puts it, the cost of proper due diligence is almost always far lower than the cost of resolving a dispute once the transaction has closed.

There is a wider point underneath this, and it belongs to him rather than to us. Asked what he looks for as a lawyer and consultant before buying, his answer is not the highest projected yield. It is the property that is simplest to operate, cleanest on zoning and licensing, clearest on title and access, and lowest on regulatory risk. In a market moving through a regulatory transition, the sustainable investment is rarely the loudest one.

The Structure Changes the Number

There is one more layer we have left deliberately for its own article. The same villa, at the same price, produces a different tax outcome depending on how the purchase is structured: an individual buying from an individual, an individual buying from a PT PMA, a company buying from a company. The structure can change the bill on an identical transaction. That is a conversation worth having before you choose, not after.

A final word on optimisation, because it is the most dangerous ground of all. Some of it is entirely legal and worth proper advice, the legitimate structuring any well-run acquisition uses. The rest, the title held quietly in a local friend’s name, the income reclassified to disappear, the value understated on the deed, is not a clever shortcut. It is the kind of arrangement that costs people millions and, at the far end, their liberty. The line between the two is exactly where a vetted legal and tax adviser earns the fee.

Knowing What to Ask

We say this often and will keep saying it. The most expensive mistake in foreign property is not knowing what to ask. Now you do. If you want these questions answered against a specific property, with verified legal and tax counsel rather than a reel, that is the conversation we are built for.

Credit:

Four Pillars Consulting

( https://fourpillarsconsulting.com/ )

CLICK HERE TO READ MORE ARTICLES ABOUT REAL ESTATE TREND IN BALI

{kind=link}